The Difference Between Personal IBANs, Corporate IBANs, and Virtual IBANs

Why the account number behind your payment matters more than you think and how a new kind of IBAN is quietly reshaping global finance

TL;DR

Personal and corporate IBANs are real bank accounts with legal ownership, deposit protection, and manual reconciliation. Virtual IBANs are programmable payment identifiers that route funds into a master account with no physical branch, no paperwork, and no onboarding delays.

The real problem virtual IBANs solve is reconciliation. Traditional IBANs force finance teams to manually match incoming transfers to customers. Virtual IBANs automate that process entirely by assigning every customer a unique payment identifier.

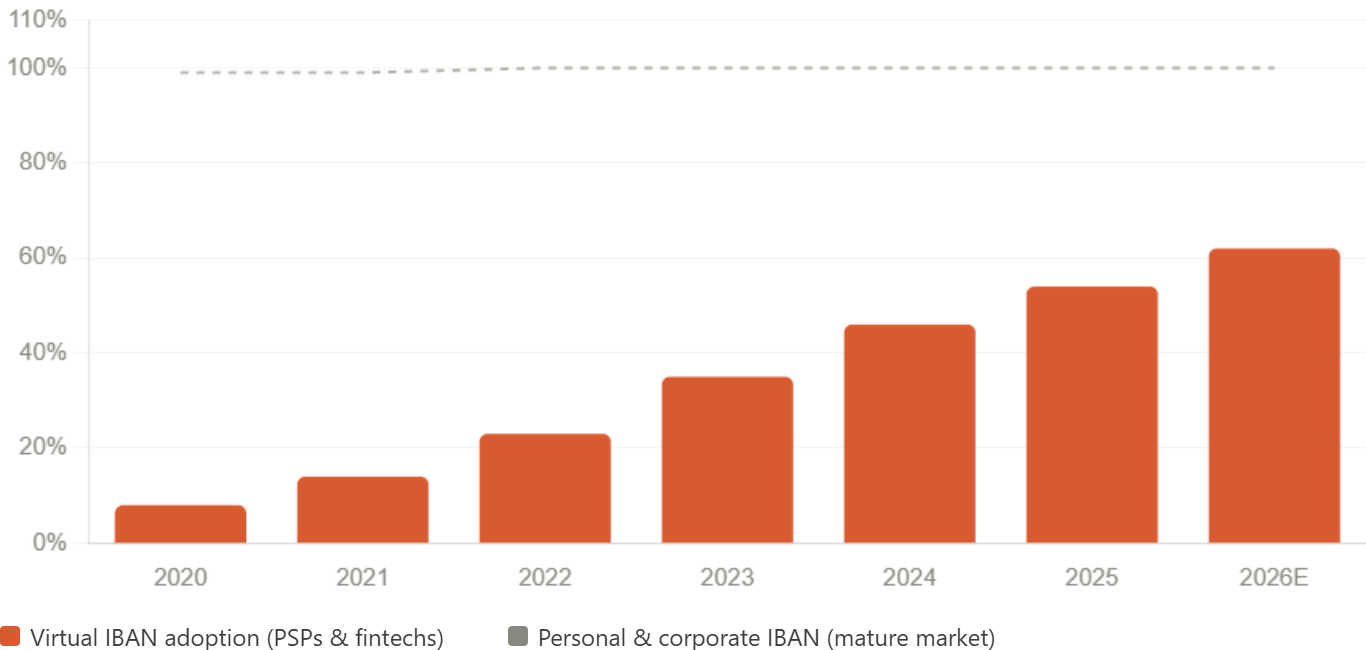

That is why adoption is exploding. Fintechs, marketplaces, and payment platforms cannot realistically open one physical bank account per user at scale.

Virtual IBANs are not fake accounts. Payments sent to them move across SEPA, SWIFT, and Faster Payments exactly like traditional bank transfers. But they introduce a different risk model: pooled funds, provider dependency, and regulatory ambiguity.

The bullish view is clear: instant issuance, automated reconciliation, multi currency collections, and infrastructure level scalability.

The bearish view is equally important: if the provider holding the master account fails, who actually controls the money?

Most people misunderstand the architecture. A virtual IBAN is not where funds live. It is the routing layer that tells the system where funds should go.

Opening Hook

It is a Tuesday afternoon in Nairobi.

A software developer named Brian has just finished a month long contract for a startup in Berlin. He sends an invoice for €2,800 and waits.

A few years ago, that payment would have taken nearly a week to arrive. Somewhere along the way, intermediary banks would shave off fees. His client’s finance team might mistype the payment reference. Brian would send follow up emails while waiting for someone in accounting to manually trace the transfer.

Today, the payment lands in under two hours.

The Berlin startup sends a standard SEPA transfer to a European IBAN issued through a Kenyan fintech called Payd, powered by infrastructure from Noah. The funds are automatically matched to Brian’s account, converted into USDC, and settled into his mobile wallet without a single human touching the process.

To the sender, the IBAN looks completely normal.

Underneath, it is an entirely different kind of financial infrastructure.

And that distinction is becoming increasingly important whether you are a freelancer getting paid globally, a founder building payment software, or a finance team processing thousands of transactions a day.

Context & The Problem

The International Bank Account Number system was standardised across Europe in the late 1990s to simplify cross border payments.

The premise was elegant: standardise account identifiers and money moves more predictably across borders.

For decades, it worked remarkably well. Today, IBANs underpin payments across Europe, the UK, and dozens of international markets. The system is trusted, mature, and deeply embedded into global banking.

But the internet changed the scale of commerce faster than banking infrastructure evolved.

Platforms now serve millions of users. Freelancers work internationally by default. Marketplaces process thousands of incoming payments every hour. And suddenly, the original IBAN model started showing strain.

The limitation is structural.

Traditional IBANs are one to one. One customer. One account. One IBAN.

That works perfectly for individuals and small businesses. It becomes operationally painful at scale.

Imagine running a marketplace with 50,000 sellers. Every day, thousands of bank transfers arrive with inconsistent references, missing invoice numbers, or sender names that do not match your records. Your finance team now spends hours manually matching payments to accounts.

At scale, reconciliation stops being an accounting task and becomes an operational bottleneck.

Virtual IBANs emerged to solve that bottleneck.

In doing so, they created an entirely new layer of financial infrastructure that most users never notice but modern fintech increasingly depends on.

System Breakdown

To understand why personal, corporate, and virtual IBANs are fundamentally different, it helps to follow how money moves through each system.

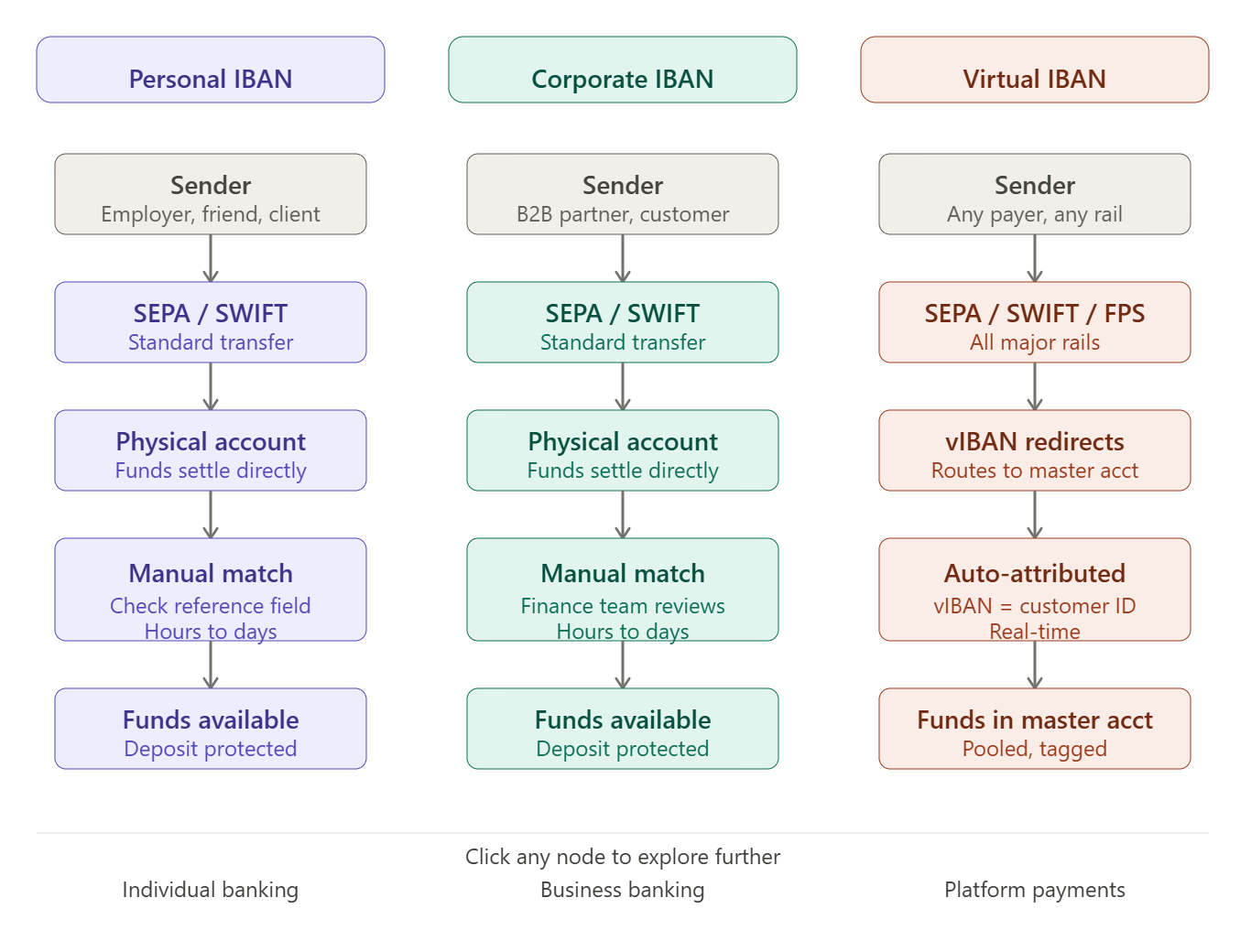

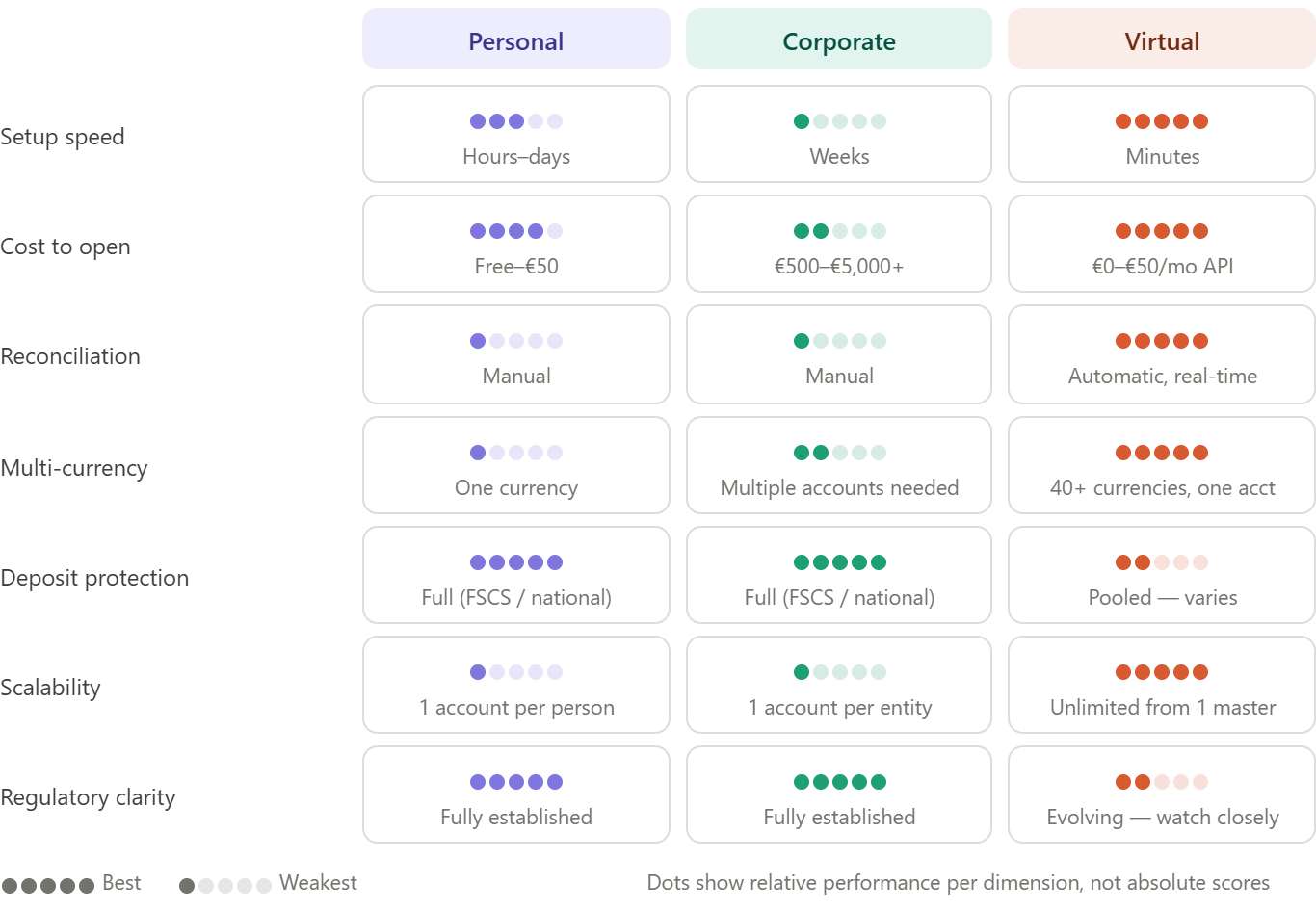

Personal IBANs are the traditional model most people know. An individual opens a bank account and receives a unique IBAN permanently tied to that account. Salary payments, transfers, and savings all sit directly inside that legal deposit account. If the bank fails, deposit protection schemes typically apply.

Corporate IBANs work similarly at the infrastructure level, but the compliance burden is significantly heavier. Businesses must complete KYB and KYC checks, provide ownership documentation, and often submit audited financials. Opening the account can take weeks and involve substantial onboarding costs.

Virtual IBANs break that model entirely.

No separate bank account is created.

Instead, a fintech or payment platform connects to a licensed banking provider through APIs and generates large volumes of unique IBANs instantly. Each virtual IBAN maps back to a single underlying master account.

When funds arrive, the system automatically identifies which virtual IBAN received the payment and attributes it to the correct customer immediately.

That distinction matters.

A personal or corporate IBAN represents an independent legal account.

A virtual IBAN is a programmable routing layer sitting on top of one.

Deep Dive

Why reconciliation is the hidden cost nobody talks about

Reconciliation sounds administrative until you operate at scale.

In reality, it is one of the most expensive and error prone processes inside modern finance operations.

Customers mistype invoice numbers. Payments arrive from unexpected accounts. Reference fields disappear during international transfers. Finance teams spend hours manually tracing money.

Virtual IBANs solve this by shifting reconciliation upstream.

Every customer receives a unique payment identifier. The moment funds arrive, attribution is already built into the system. No manual matching required.

At 10,000 transactions a month, that is not a convenience feature.

It is the difference between a lean finance operation and a bloated one.

How the infrastructure actually works

Behind every virtual IBAN sits a chain of licensed financial entities.

At the top are regulated banks or Electronic Money Institutions such as Banking Circle, Wise, Airwallex, or Modulr. These institutions hold the real accounts and regulatory licences.

Below them sit fintechs and PSPs accessing that infrastructure through APIs.

Then come the end users receiving virtual IBANs.

The model is efficient, scalable, and capital light.

But it also concentrates risk.

If a banking partner terminates a relationship with a PSP, every virtual IBAN connected to that infrastructure can stop functioning immediately. That has already happened multiple times across Europe and the UK following regulatory reviews.

Multi currency is where virtual IBANs become transformative

Traditional banking handles multiple currencies poorly.

Receiving EUR, USD, and GBP separately often requires opening multiple bank accounts across different jurisdictions, each with its own onboarding, compliance, and reconciliation workflow.

Virtual IBAN infrastructure compresses all of that into a single system.

Platforms like Wise or Airwallex can issue local receiving accounts across dozens of currencies while routing everything into one ledger environment.

What previously required a global banking footprint now requires an API integration.

Key Metrics

Personal IBANs are best for individuals and everyday banking

Corporate IBANs are built for regulated business operations

Virtual IBANs are designed for scalable payment infrastructure

Personal and corporate IBANs are real bank accounts

Virtual IBANs route payments into a master account

Traditional IBANs require manual reconciliation

Virtual IBANs automate reconciliation instantly

Personal IBANs are quick to open

Corporate IBANs require heavy compliance checks

Virtual IBANs can be issued instantly via APIs

Corporate banking is expensive and documentation heavy

Virtual IBAN infrastructure is cheaper and highly scalable

Traditional IBANs are limited for multi currency collections

Virtual IBANs support global payments across multiple currencies

Personal and corporate IBANs usually include deposit protection

Virtual IBAN protection depends on the provider structure

Virtual IBAN adoption is growing rapidly across fintech and marketplaces

Risks

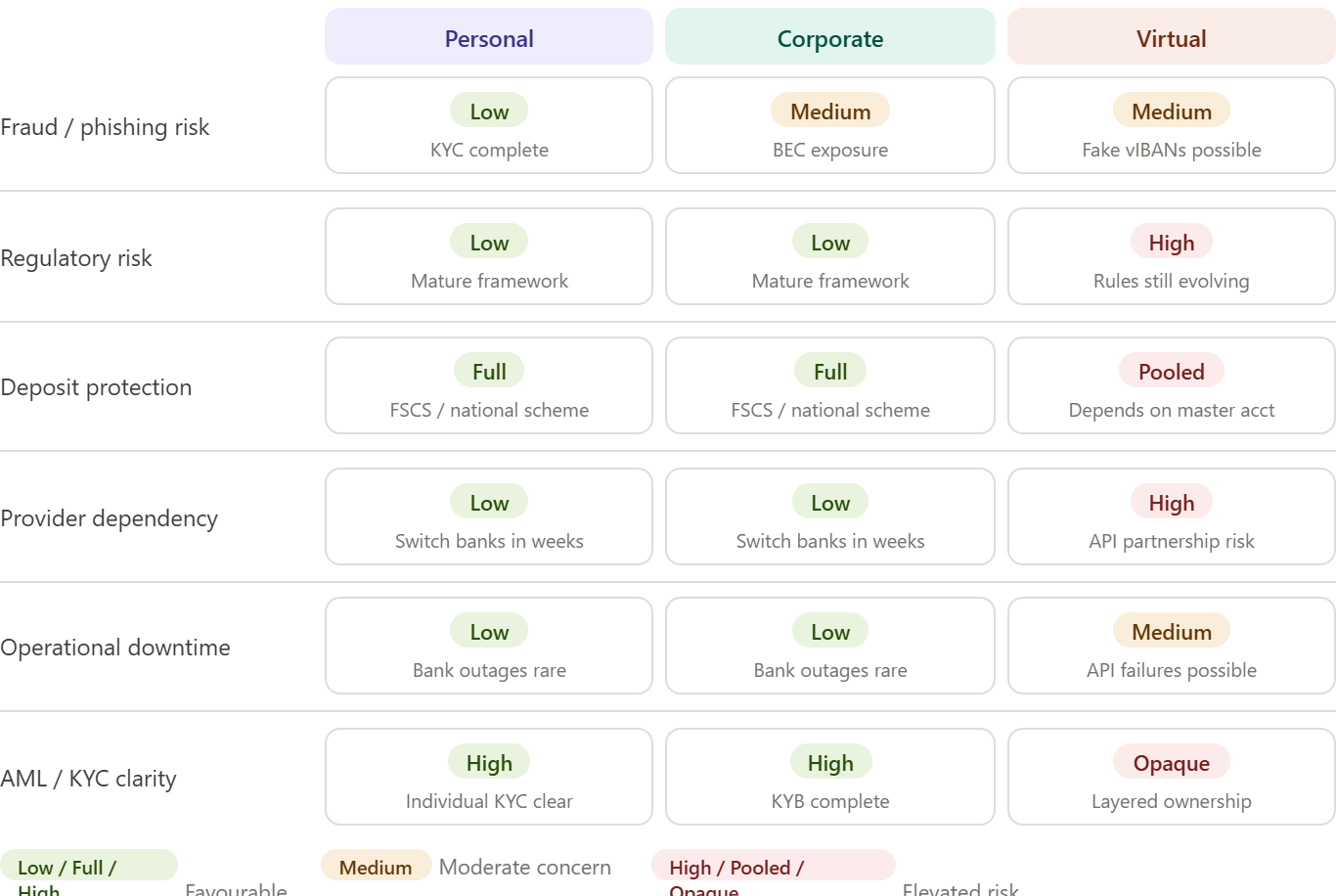

Custodial risk is the issue sophisticated finance teams focus on

Virtual IBANs typically point to pooled master accounts.

That means users may not hold individually ring fenced deposit accounts in the traditional sense.

If the provider holding the master account freezes operations or fails, access to funds can become delayed or uncertain.

That risk is not hypothetical. Several European e money institutions collapsed over the past decade, exposing how fragile pooled structures can become under stress.

Regulation is catching up

AML frameworks were built around direct account ownership.

Virtual IBAN structures complicate that assumption because the end user may sit multiple layers away from the institution holding the underlying account.

Regulators across Europe and the UK are increasingly scrutinising this model. Expect tighter rules around transparency, traceability, and ring fencing over the next few years.

Fraud risk cuts both ways

Virtual IBANs look identical to traditional ones.

That makes them operationally seamless but also attractive for fraud schemes such as business email compromise attacks.

At the same time, dynamic and transaction specific virtual IBANs can dramatically reduce fraud exposure by making account identifiers temporary and non reusable.

The technology increases both flexibility and responsibility.

Provider dependency is underestimated

Traditional businesses can migrate between banks gradually.

Platforms built entirely on a virtual IBAN provider’s APIs cannot move nearly as easily.

If pricing changes, services are restricted, or banking relationships break down, entire payment flows can fail overnight.

Infrastructure abstraction creates efficiency.

It also creates dependency.

Bull vs Bear Case

Bull Case: Virtual IBANs become the default operating layer for business payments

The momentum is difficult to ignore.

Every marketplace, SaaS platform, payroll provider, and fintech eventually encounters the same scaling problem: reconciliation.

Virtual IBANs solve it elegantly.

As infrastructure matures, many of today’s risks become manageable. Named virtual IBANs improve traceability. Providers are becoming larger and better capitalised. Regulatory frameworks are slowly adapting to support rather than resist the model.

In this world, virtual IBANs become invisible infrastructure by the end of the decade. Every serious payment platform runs on them whether users notice or not.

Bear Case: Consolidation and regulation weaken the model

The concerns regulators have are legitimate.

If virtual IBAN providers are forced to hold bank level capital requirements or perform full KYC at every virtual account level, the speed and cost advantages shrink quickly.

At the same time, the market is consolidating around a small number of providers.

That creates systemic concentration risk. A major provider failure could ripple through thousands of platforms simultaneously.

The architecture scales beautifully.

The dependency chain may not.

Scenario Analysis

Scenario 1: You are a freelancer working globally

A traditional domestic bank account is increasingly inefficient for cross border work.

Platforms like Wise, Payoneer, or Airwallex allow freelancers to receive local payments across multiple currencies without paying repeated SWIFT and FX penalties.

For millions of global freelancers, virtual IBAN infrastructure is already the rational default.

Scenario 2: You are building a marketplace

At scale, reconciliation becomes existential.

If thousands of sellers send payments into a shared account with inconsistent references, operational complexity compounds rapidly.

Virtual IBANs solve this cleanly by assigning every seller a dedicated payment identifier.

Without them, scaling becomes painful.

Scenario 3: You are a CFO managing international operations

The optimal structure is usually hybrid.

Corporate IBANs provide legal robustness for treasury and operating balances.

Virtual IBANs provide scalable collections infrastructure across currencies and jurisdictions.

One delivers protection.

The other delivers operational leverage.

Scenario 4: You are a regulator reviewing a fintech

The questions become straightforward:

Who controls the master account?

How are funds safeguarded?

What happens if the provider exits?

How transparent is beneficial ownership?

Those questions are increasingly defining the next generation of payments regulation.

What Most People Miss

“Virtual” does not mean less real

Payments sent to virtual IBANs travel through the same payment rails as traditional transfers.

SEPA remains SEPA.

SWIFT remains SWIFT.

The difference is not in how the payment moves.

It is in how the infrastructure behind the payment is designed.

The real innovation is not the IBAN itself

The IBAN is simply the interface.

The real product is the reconciliation engine, the ledger infrastructure, and the automation layer sitting underneath it.

That is what businesses are actually paying for.

Corporate IBANs are not just business versions of personal accounts

The compliance burden is fundamentally different.

Corporate banking involves ownership verification, regulatory reporting, and legal accountability at a much deeper level than personal banking.

The payment mechanics may look similar.

The regulatory architecture is not.

Dynamic virtual IBANs may reduce fraud significantly

One time virtual IBANs become useless after payment completion.

That changes the economics of fraud entirely.

Some providers already report major reductions in payment diversion attacks after shifting from static account details to dynamically generated identifiers.

Key Variables

The usefulness of each IBAN type depends on four variables:

Transaction volume

Low volume businesses can manage manual reconciliation. High volume businesses eventually cannot.Geographic footprint

Single market businesses can operate comfortably with traditional accounts. Multi currency businesses gain disproportionate value from virtual IBAN infrastructure.Regulation

The regulatory environment around virtual IBANs is still evolving rapidly, particularly in Europe.Provider quality

Infrastructure is only as reliable as the institution behind it. Capitalisation, licensing, and banking partnerships matter enormously.

Strategic Impact

For fintechs, virtual IBANs are no longer a differentiator.

They are foundational infrastructure.

For banks, they represent both competitive pressure and a new monetisation layer. Institutions that expose virtual IBAN capabilities through APIs effectively turn banking licences into infrastructure products.

For regulators, virtual IBANs sit at the centre of a growing oversight challenge involving pooled funds, beneficial ownership visibility, and systemic dependency.

For businesses and individuals, the decision is ultimately practical:

Personal IBANs for everyday banking.

Corporate IBANs for legal and operational robustness.

Virtual IBANs for scale, automation, and global payment flexibility.

Conclusion

Personal IBANs, corporate IBANs, and virtual IBANs are not upgraded versions of one another.

They solve different problems.

Personal IBANs were built for individuals.

Corporate IBANs were built for regulated business banking.

Virtual IBANs were built for a world where payments move faster than manual operations can keep up.

That distinction matters because finance is quietly shifting from account based infrastructure to programmable infrastructure.

The IBAN on the surface still looks familiar.

But underneath, the system is changing.

Brian in Nairobi receiving euros in hours instead of days is not just a better user experience. It is evidence that a new financial operating layer is forming on top of legacy banking rails.

Most people will never notice the transition.

But the companies building global payment systems already have.

And increasingly, the winners will be the ones who understand the infrastructure beneath the account number.

Personal Note

What makes the virtual IBAN story interesting is not the complexity of the technology.

It is how quietly it changes the assumptions banking was built on.

For decades, financial infrastructure assumed accounts and identities were tightly linked. One person. One account. One permanent identifier.

Virtual IBANs separate those layers.

The account stays in one place while programmable identifiers move dynamically on top of it.

To the outside world, nothing changes. The payment still looks like a normal bank transfer.

But underneath, the architecture becomes dramatically more flexible, scalable, and software driven.

That pattern shows up repeatedly in infrastructure revolutions. The interface remains familiar while the underlying system changes completely.

The IBAN typed into a payment form today may represent a traditional bank account opened decades ago or a virtual identifier generated seconds earlier through an API.

Same interface.

Entirely different economics.

And increasingly, the virtual model is winning on speed, scalability, and cost.